Key highlights

- 2022 was the third best year ever for new capacity with 78 GW added globally.

- Total installed global capacity grew to 906 GW. This represents Year-on-Year growth of 9%.

- 2023 should be the very first year to exceed 100 GW of new capacity added globally with this on same fact GWEC Market Intelligence forecasts year-on-year growth of 15%.

- GWEC Market Intelligence forecasts 680 GW of new capacity in the next five years (2023-27). This represents 136 GW per year to 2027.

- GWEC Market Intelligence has a positive outlook up to 2030, with an additional 143 GW expected by the end of the decade, 13% higher than previous forecasts. We previously forecast 1078 GW to be built from 2022-2030, this is now forecast to be 1221 GW of new capacity added between 2023-2030.

New installations (GW)

Globally, 77.6 GW of new wind power capacity was connected to power grids in 2022, bringing total installed wind capacity to 906 GW1, a growth of 9% compared with 2021.

The world’s top five markets for new installations in 2022 were:

- China

- USA

- Brazil

- Germany

- Sweden

Altogether, they made up 71% of global installations last year, collectively 3.7% lower than 2021. This was primarily due to the world’s two largest markets, China

and the US, losing a combined 5% market share compared with the previous year – the second consecutive year that both countries have lost market share.

Regional onshore and offshore wind outlook for new installations (GW)

North America

In total, 60 GW of onshore wind capacity is expected to be added in the next five years in North America, of which 92% will be built in the US and the rest in Canada.

Europe

With strong growth coming back in established European markets such as Germany, Spain, the UK, France, Italy and Turkey, the European onshore market will take off again from 2024.

Africa/Middle East

In total, 17 GW of new capacity is expected to be added in the next five years (2023–2027), of which 5.3 GW will come from South Africa, 3.6 GW from Egypt, 2.4 GW from Saudi Arabia and 2.2 GW from Morocco.

Latin America

GWEC Market Intelligence expects 26.5 GW of onshore wind to be added in this region in the next five years with Brazil, Chile and Colombia contributing 78% of the additions.

The 2 TW milestone is expected to be achieved in just seven years

Compared with the 2030 global outlook released alongside last year’s Global Wind Report, GWEC Market Intelligence has increased its forecast for total wind power capacity additions for 2023–2030 by 143 GW (13% YoY).

The main reasons behind this upgrade include:

- Energy system reform in Europe, replacing fossil fuels with renewables to achieve energy security in the aftermath of Russia’s invasion of Ukraine;

- China’s commitment to further expand the role of renewables in its energy mix;

- An anticipated ten-year installation uplift in the US, driven by the passage of the IRA.

Onshore wind demand and supply benchmark, 2023-2031 (MW)

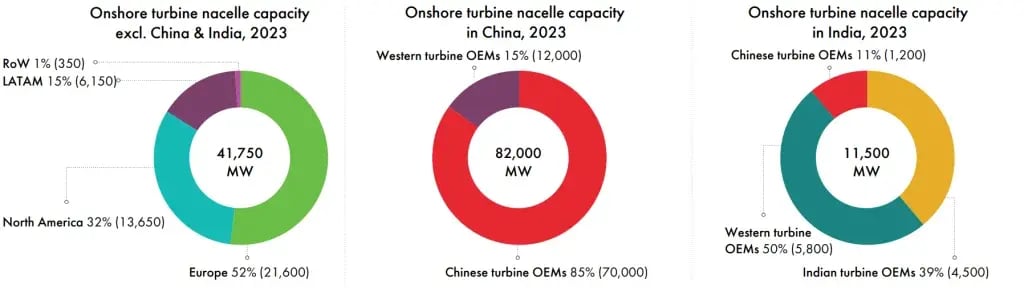

China dominates global onshore wind turbine nacelle assembly with 82 GW of identified annual capacity. With 21.6 GW of annual assembly capacity per annum, Europe is the world’s second largest onshore turbine nacelle production base, followed by the US (13.6 GW), India (11.5 GW) and LatAm (6.2 GW).

We conclude that the supply chain in China, India and LATAM will have enough nacelle production capacity to accommodate demand, while the rest of world, in a business as usual scenario, will continue to rely on imported wind turbines to cope with the anticipated growth.

Offshore wind demand and supply benchmark, 2023–2031 (MW)

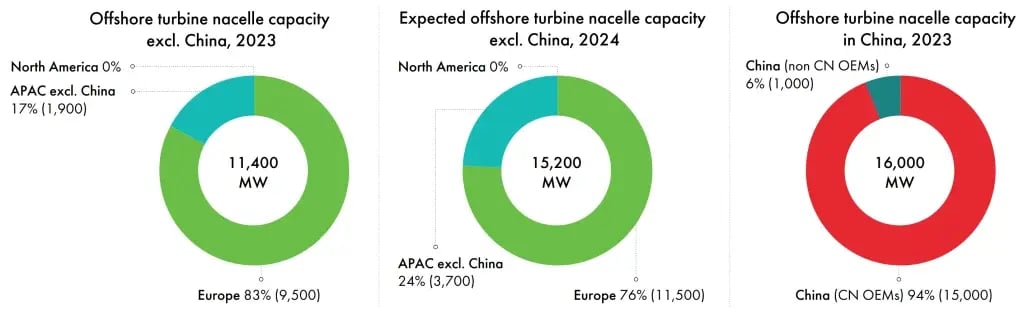

Compared with onshore wind, the supply chain for offshore wind turbines is more concentrated, due to the fact that more than 99% of total global offshore wind installation is presently located in Europe and the APAC region.

China is the world’s number-one offshore turbine nacelle production centre with annual assembly capacity of up to 16 GW, of which 1 GW is owned by one western turbine OEM.

Media enquiries

Alex Bath

Communications Director

-

alex.bath@gwec.net